Downsize Home Fast Cash Offer: Your 2026 Guide

TL;DR:

- A downsize home fast cash offer is an all-cash bid that buys your property as-is, providing certainty for homeowners under pressure. To sell quickly, homeowners should prepare essential documents, verify buyer legitimacy, and understand the impact of property condition on offers. The process ensures a rapid closing in 7 to 14 days, with cash offers reflecting market value minus typical discounts for speed and risks.

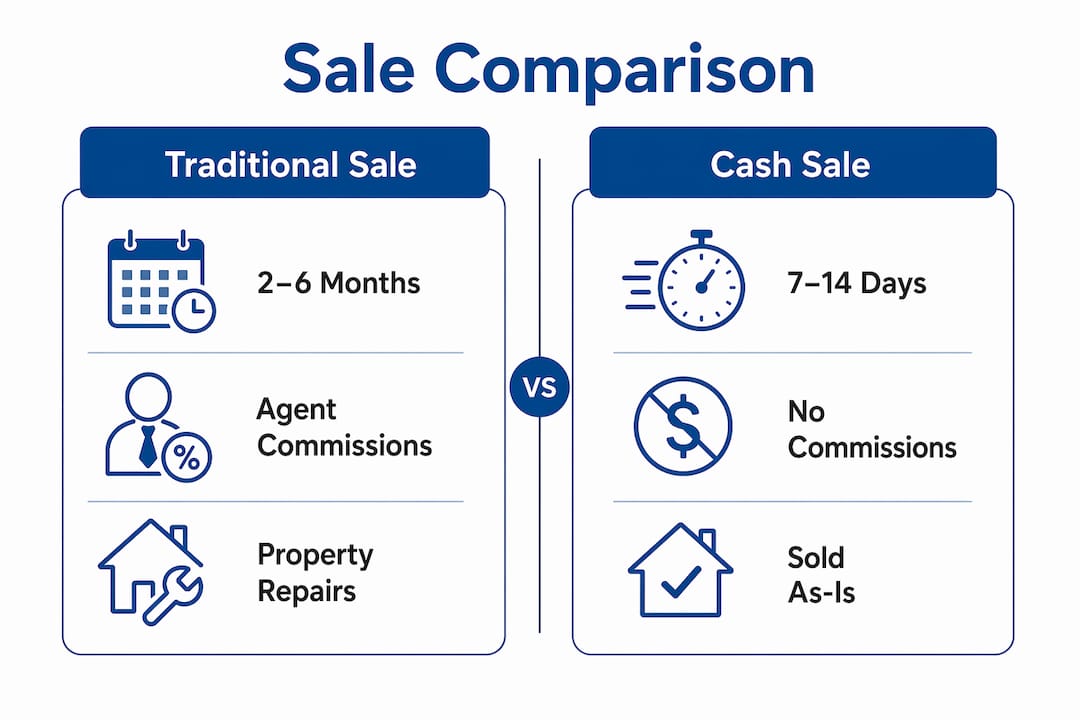

A downsize home fast cash offer is a direct, all-cash bid from a buyer who purchases your property as-is, without financing contingencies, repairs, or lengthy market exposure. For homeowners facing financial pressure, foreclosure, or a tight deadline, this approach delivers something traditional sales rarely can: certainty. Cash sales close in 1–3 weeks, compared to 2–6 months for a financed transaction. That gap is the entire reason fast cash for downsizing has become the preferred exit for homeowners who cannot afford to wait. The industry term for this transaction type is a “direct cash purchase,” and understanding how it works puts you in control from the first phone call.

What do you need before pursuing a downsize home fast cash offer?

Preparation separates a smooth closing from a stalled one. Before you contact any cash buyer, gather the documents and information that buyers will request immediately.

Documents and property information to have ready

- Proof of ownership: Your deed or title document confirms you have the legal right to sell.

- Mortgage payoff statement: Contact your lender for a current payoff amount so you know your net proceeds before accepting any offer.

- Property tax records: Buyers check for outstanding tax liens, which can delay or kill a closing.

- HOA documents: If your home is in a homeowners association, provide the current fee schedule and any outstanding balances.

- Recent utility bills: These help buyers assess the property’s operating costs and condition.

Understanding how property condition affects your offer

Cash buyers price their offers based on condition. A home needing a new roof or foundation work will receive a lower bid than one in good shape. The good news is that sellers avoid costly repairs entirely with a cash sale, since buyers purchase as-is and factor renovation costs into their offer. You do not need to fix anything before selling.

How to evaluate offers and verify buyer legitimacy

Always request proof of funds in writing before signing anything. A legitimate cash buyer provides a bank statement or letter from a financial institution confirming available funds. A legitimate cash offer includes few or no contingencies and is backed by verified funds, unlike some wholesaler offers that depend on finding a third-party buyer. Use a free home valuation from a source like Gregg Perrah’s valuation tool to establish a baseline before comparing offers.

| Prerequisite | Why it matters |

|---|---|

| Deed or title document | Confirms legal ownership and speeds title search |

| Mortgage payoff statement | Reveals your true net proceeds after sale |

| Proof of funds from buyer | Protects against scams and deal collapses |

| Property tax records | Uncovers liens that could delay closing |

| HOA documents | Prevents surprise fees at closing |

How do you sell your home quickly with a cash offer?

The process is straightforward once you know each step. Here is the exact sequence from first contact to closing day.

-

Contact reputable cash buyers and request offers. Reach out to two or three buyers to create light competition. Sell Dave Your House, for example, delivers a no-obligation offer within 24 hours of evaluating your property.

-

Review and compare no-obligation offers. Read each offer carefully. Check the purchase price, any remaining contingencies, and the proposed closing date. A no-obligation offer means you can walk away without penalty if the terms do not work for you.

-

Accept the offer and open escrow. Once you sign the purchase agreement, the buyer’s title company opens escrow and orders a title search. Title searches take 1–5 business days and are the most common bottleneck in a cash closing. Resolving any liens or probate gaps before this stage saves significant time.

-

Skip repairs and staging. Because the sale is as-is, you do not hire contractors, stage rooms, or schedule open houses. An as-is sale speeds downsizing by removing weeks of preparation that traditional listings require.

-

Close on your timeline. Cash closings typically happen in 7–14 days. Remote closing via mobile notary is available in most states, so you do not need to appear in person at a title office. On closing day, you sign the transfer documents, the buyer wires funds, and the sale is complete.

Pro Tip: Request that the title company order the title search the same day you sign the purchase agreement. That single action can shave two to three days off your closing timeline.

The absence of mortgage underwriting and appraisal requirements is what makes this speed possible. Cash offers eliminate financing risk and the contingencies that cause 30–45 days of delay in financed transactions. You skip the bank’s timeline entirely.

How do you handle common challenges when selling fast for cash?

Speed creates pressure, and pressure creates mistakes. Knowing the pitfalls before you encounter them keeps your sale on track.

- Discounted offers below expectations. Cash buyers typically offer 70%–85% of fair market value. That range reflects their carrying costs and renovation budget, not a judgment on your home’s worth. Set your expectations before you receive the first offer.

- Title issues and liens. Outstanding property tax debt, contractor liens, or unresolved probate can pause a closing for weeks. Pull a preliminary title report early to identify problems while you still have time to resolve them.

- Rushed decisions under financial stress. Urgency is real, but signing the first offer you receive without comparison is a costly habit. Getting at least two offers takes less than 48 hours and gives you negotiating leverage.

- Unverified buyers. Wholesalers sometimes present offers they cannot fund independently. Always confirm proof of funds before proceeding.

- Emotional attachment clouding judgment. Downsizing is personal. Separating the financial decision from the emotional one protects your net proceeds.

“Sellers should secure a cash offer first as a baseline before exploring other options, to better negotiate and set expectations.” — Distressed Property Solutions

That advice is practical, not just strategic. A confirmed cash offer in hand gives you a floor price. Any other option you explore must beat that floor to be worth the extra time and risk.

What financial trade-offs should you expect with fast cash offers?

The core trade-off in any quick home sale is price versus speed. Understanding the numbers clearly helps you decide whether a cash sale fits your situation.

Cash buyers typically offer 70%–85% of a home’s fair market value. That discount compensates them for buying without inspection contingencies, taking on renovation costs, and absorbing carrying costs while they prepare the property for resale. The discount is not arbitrary. It is the price of speed and certainty.

The net proceeds comparison, however, is less dramatic than the headline discount suggests. Cash sales can net sellers $8,600–$22,000 less than a traditional sale, but they close 3–4 months faster. When you factor in agent commissions (typically 5%–6%), repair costs, staging fees, and monthly holding costs like mortgage payments and insurance, the gap narrows considerably.

| Factor | Traditional sale | Cash sale |

|---|---|---|

| Closing timeline | 2–6 months | 7–14 days |

| Agent commissions | 5%–6% of sale price | None |

| Repair and staging costs | $3,000–$15,000+ | $0 |

| Financing fall-through risk | High | None |

| Net proceeds vs. list price | Higher gross, lower net | Lower gross, higher net certainty |

For distressed or time-constrained sellers, cash offers provide certainty that a traditional listing simply cannot match. A financed buyer can lose their mortgage approval the week before closing, sending you back to square one. A cash buyer cannot. That reliability has real financial value, especially when you are managing debt, a job relocation, or an inherited property you cannot maintain.

The cash home sale benefits go beyond the closing check. You also avoid months of mortgage payments, utility bills, and insurance premiums on a home you no longer want to own. For many homeowners, those savings close the gap between a cash offer and a traditional sale price.

Key Takeaways

A fast cash offer is the most reliable way to downsize quickly, trading a modest price discount for certainty, speed, and zero repair costs.

| Point | Details |

|---|---|

| Cash sales close fast | Expect closing in 7–14 days, compared to 2–6 months for traditional sales. |

| Offers reflect market reality | Cash buyers typically offer 70%–85% of fair market value to cover renovation and carrying costs. |

| Net proceeds gap is smaller than it looks | Savings on commissions, repairs, and holding costs reduce the actual price difference significantly. |

| Title issues are the main delay | Order a preliminary title report early to resolve liens or probate gaps before they stall closing. |

| Verify every buyer | Always request written proof of funds before signing any purchase agreement. |

What I’ve learned after years of watching homeowners downsize under pressure

The biggest mistake I see is homeowners fixating on the gross offer price instead of the net proceeds. A $200,000 cash offer on a home listed at $220,000 feels like a loss. But subtract a $13,200 agent commission, $8,000 in repairs the buyer demanded, two months of mortgage payments, and the math shifts fast. The cash offer often wins on net, and it always wins on certainty.

The second mistake is waiting too long to get a cash offer. Homeowners often treat it as a last resort, something to consider only after a listing fails. That is backwards. Getting a fair cash offer first costs you nothing and gives you a baseline. Every other option you explore gets measured against it.

I have also seen homeowners walk away from legitimate cash buyers because the offer felt low, only to accept the same number three months later after carrying costs and stress piled up. Speed has a dollar value. Certainty has a dollar value. The homeowners who recognize that early make better decisions and sleep better at night.

Choose buyers with a verifiable track record, not just a website. Ask for references. Confirm proof of funds. And remember that a slightly lower offer from a trustworthy buyer beats a higher number from someone who cannot close.

— Real Estate Team

How Sell Dave Your House delivers fast cash offers in Detroit

Sell Dave Your House has worked with Detroit-area homeowners for over 16 years, providing no-obligation cash offers within 24 hours and closings in as little as seven days.

You pay no agent commissions, no repair costs, and no hidden fees. The process is designed for homeowners who need to move quickly, whether you are facing foreclosure, managing an inherited property, or simply ready to downsize without the burden of a traditional listing. Sell Dave Your House buys homes as-is, in any condition, on a timeline that works for you. If you are ready to see what your home is worth, get a cash offer today or learn more about fast cash sales in Detroit to take the first step toward a clean, fast closing.

FAQ

How fast can I close with a cash home buyer?

Cash sales typically close in 7–14 days, compared to 2–6 months for a traditional financed sale. The exact timeline depends on how quickly the title search is completed.

Will a cash buyer purchase my home as-is?

Yes. Cash buyers purchase properties in any condition, so you do not need to make repairs or stage the home before selling.

How much below market value will a cash offer be?

Cash buyers typically offer 70%–85% of fair market value. The discount reflects the buyer’s renovation costs and the speed and certainty they provide.

What is the biggest risk in a fast cash sale?

The main risk is accepting an offer from an unverified buyer. Always request written proof of funds before signing a purchase agreement to confirm the buyer can actually close.

Can I sell my home for cash if I have a mortgage?

Yes. Your mortgage is paid off at closing from the sale proceeds. Request a current payoff statement from your lender before accepting any offer so you know your exact net proceeds.