Home sale proceeds planning is the intentional process of managing the net funds you receive after selling your home to protect your financial security and meet your short and long-term goals. Most homeowners focus on the sale price but overlook the gap between that number and what actually lands in their bank account. Selling costs, mortgage payoffs, taxes, and transition expenses all reduce your take-home amount. Understanding home sale proceeds management before you close gives you the power to make confident, informed decisions with every dollar you receive.

What is home sale proceeds planning and why does it matter?

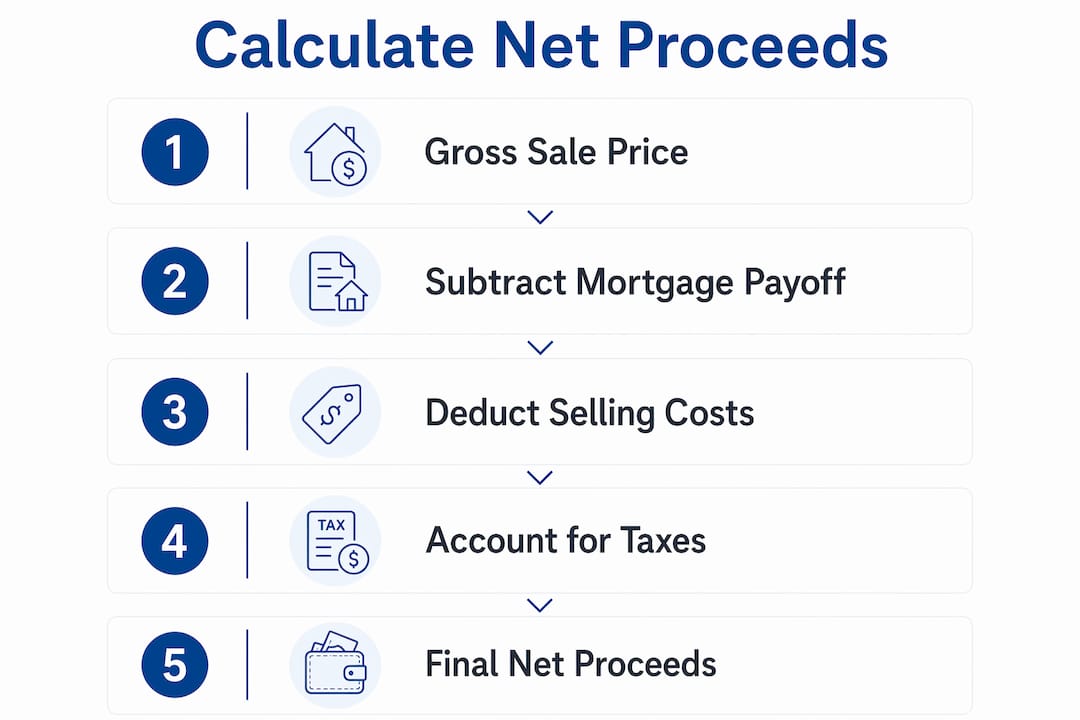

Home sale proceeds planning is the structured approach to calculating, protecting, and allocating the net money from a property sale. The industry term for the funds you receive is “net proceeds,” which equals your gross sale price minus your mortgage payoff and all selling costs. Net proceeds are typically 7 to 10% less than the sale price. That gap can represent tens of thousands of dollars on a median-priced home.

Planning matters because the decisions you make in the days and weeks after closing have lasting financial consequences. Sellers who treat proceeds as a windfall often misallocate funds, miss tax deadlines, or fail to cover transition costs. A clear plan prevents those mistakes before they happen.

How to calculate net home sale proceeds accurately

Gross sale price minus mortgage payoff and selling costs equals your net proceeds. Agent commissions and closing fees are the largest typical deductions. Knowing each line item before closing removes surprises.

The table below shows the most common cost categories and their typical ranges:

| Cost category | Typical range |

|---|---|

| Real estate agent commissions | 3 to 6% of sale price |

| Transfer taxes | 0.1 to 2% of sale price |

| Title insurance | $500 to $2,000 |

| Escrow and settlement fees | $500 to $1,500 |

| Total estimated selling costs | 7 to 10% of sale price |

Your mortgage payoff is separate from these fees. Contact your lender for a payoff statement that reflects the exact balance on your closing date, including any prepayment penalties. Home sale proceeds calculators show line-item amounts so you can build accurate profit expectations before you sign anything.

The method you use to sell also affects your net. Agent-assisted sales carry the highest commission costs. For Sale By Owner (FSBO) eliminates agent fees but adds marketing and legal work. Cash buyers like Sell Dave Your House charge no commissions and cover closing costs, which can meaningfully increase your net proceeds.

What are the tax implications of home sale proceeds?

Capital gains tax is the primary tax concern for most home sellers. Your taxable gain equals your sale price minus your cost basis, which is your original purchase price plus the cost of qualifying home improvements. Verifying your cost basis and mortgage payoff before finalizing your plan is a step many sellers skip, and it directly affects both your net proceeds and your tax bill.

The IRS provides significant relief for primary residence sellers through the capital gains exclusion:

- Single filers can exclude up to $250,000 in capital gains from federal tax.

- Married couples filing jointly can exclude up to $500,000 in capital gains on a primary residence sale.

- You must have lived in the home for at least two of the last five years to qualify.

- Gains above the exclusion threshold are taxed at long-term capital gains rates (0%, 15%, or 20% depending on income).

State taxes add another layer. Washington state, for example, imposes a 7% capital gains tax on gains above the federal exclusion. Your state may have its own rules, so check with a local tax professional. High-income sellers should also be aware that the 3.8% Net Investment Income Tax may apply to significant capital gains after the exclusion.

One often-overlooked detail: major home improvements adjust your cost basis upward, which reduces your taxable gain. Keep records of renovations, additions, and system replacements. Estate planning also intersects here. Heirs may benefit from a step-up in basis if a sale is deferred until after death, which can significantly reduce taxable gains for the next generation.

Smart strategies for managing and allocating home sale proceeds

Financial experts recommend a four-part framework for home sale proceeds distribution that balances safety, growth, and income needs. The right mix depends on your age, income, debt load, and upcoming expenses.

- Build an emergency fund first. Set aside three to six months of living expenses in a liquid account before allocating anything else. This protects you if unexpected costs arise during your transition.

- Pay down high-interest debt. Eliminating credit card balances or personal loans with double-digit interest rates delivers an immediate, guaranteed return that most investments cannot match.

- Invest for long-term growth. Once your safety net is in place, consider diversified investments aligned with your risk tolerance. Stocks, index funds, and real estate investment trusts (REITs) are common options.

- Supplement retirement income. Annuities can convert a lump sum into a predictable income stream, which is valuable for retirees without a pension.

High-yield savings accounts and money market accounts offer liquidity with better interest rates, making them well-suited for funds you will need within 18 to 24 months. Parking proceeds in one of these accounts while you finalize your long-term plan is a practical first step.

One critical warning: avoid annuitizing your entire proceeds immediately. Retain enough liquidity to cover moving expenses, new home setup costs, and unexpected repairs. Annuitize only the portion needed to cover essential income, and keep the rest flexible.

What to consider when transitioning after selling your home

Home sale proceeds should be viewed within a broader life transition context. Failing to plan for secondary expenses leads to misallocation of funds and cash flow problems that catch sellers off guard. The sale is not the finish line. It is the starting point for a new financial chapter.

Key transition costs to plan for include:

- Moving and relocation costs. Professional movers, storage units, and travel expenses add up quickly, especially for long-distance moves.

- New home purchase or rental deposits. If you are buying again, you will need funds for a down payment, inspection fees, and closing costs. Renters face first and last month's rent plus security deposits.

- Insurance updates. Homeowner's insurance, renter's insurance, and umbrella policies all need to be reviewed and updated.

- Temporary income gaps. If your sale coincides with a job change or retirement, plan for a period with reduced income.

- Estate and inheritance planning. If you are selling a family home or an inherited property, proceeds may need to be distributed among heirs or held in trust.

A fee-only fiduciary advisor provides personalized financial plans that account for all of these factors. For proceeds over $300,000, a financial plan costing $3,000 to $5,000 can pay for itself within three meetings. That is not an expense. It is an investment in getting the rest of your decisions right.

Key takeaways

Home sale proceeds planning requires calculating your true net proceeds, managing tax exposure, and allocating funds across emergency reserves, debt reduction, and long-term investments before you spend a single dollar.

| Point | Details |

|---|---|

| Net proceeds are less than sale price | Selling costs of 7 to 10% reduce what you actually receive at closing. |

| Tax exclusions reduce your bill | Single filers exclude up to $250,000; married couples exclude up to $500,000 in capital gains. |

| Liquidity comes first | Build an emergency fund and cover transition costs before investing or annuitizing proceeds. |

| Fiduciary advice pays off | A fee-only advisor for proceeds over $300,000 typically covers their cost within three sessions. |

| Track cost basis adjustments | Home improvements raise your cost basis and lower your taxable gain, saving you real money. |

What I've learned from watching homeowners handle proceeds well and poorly

Most homeowners I've worked with in the Detroit area treat closing day as the end of the process. It is actually the beginning of the most financially consequential decisions they will make. The sellers who come out ahead are the ones who started planning two to three months before closing, not two to three days after.

The biggest mistake I see is skipping the fiduciary advisor because the fee feels unnecessary. That thinking is backwards. A fee-only advisor has no incentive to sell you a product. They tell you what actually fits your situation. For anyone receiving a significant lump sum, that objectivity is worth far more than the cost.

I also see sellers overlook basis adjustments consistently. If you replaced your roof, added a bathroom, or finished a basement, those costs raise your cost basis and reduce your taxable gain. Most people never document this properly, and they pay more in taxes than they should.

One more thing: do not let urgency push you into permanent decisions. The cash sale process can close in days, which is genuinely useful when you need liquidity fast. But fast access to proceeds does not mean you should deploy those funds fast. Slow down after the sale. The money will still be there when you have a real plan.

— Dave Joseph, Owner of Sell Dave Your House

How Sell Dave Your House helps you access proceeds faster

If you are a Detroit-area homeowner who needs to sell quickly and get clean access to your proceeds, Sell Dave Your House offers a direct path. With over 16 years of experience buying homes for cash in Michigan, the team provides fair all-cash offers within 24 hours and can close in as little as seven days. There are no agent commissions, no repair requirements, and no hidden fees eating into your net proceeds.

Fast access to your proceeds gives you more time and flexibility to plan their allocation properly. Whether you are selling a house fast in Detroit or looking to close quickly in Harper Woods, Sell Dave Your House makes the process straightforward. Get a cash offer today and start your proceeds planning from a position of clarity.

FAQ

What does home sale proceeds planning mean?

Home sale proceeds planning is the process of calculating your net proceeds after selling costs and taxes, then allocating those funds to meet your financial goals. It covers everything from emergency reserves to retirement income and debt payoff.

How much do selling costs reduce my proceeds?

Selling costs typically reduce proceeds by 7 to 10% of the sale price, covering agent commissions, transfer taxes, title insurance, and escrow fees. Cash sales with buyers like Sell Dave Your House eliminate agent commissions entirely.

Do I owe taxes on my home sale proceeds?

Most primary residence sellers owe no federal capital gains tax thanks to the $250,000 exclusion for single filers and the $500,000 exclusion for married couples. Gains above those thresholds are taxable, and state taxes may also apply.

When should I consult a financial advisor about my proceeds?

Consult a fee-only fiduciary advisor before your closing date, not after. Pre-sale planning gives you options for managing tax liability and allocating funds that post-sale advice cannot recover.

What is the safest place to put home sale proceeds short term?

High-yield savings accounts and money market accounts are the safest short-term options. They offer liquidity and better interest rates than standard checking accounts, making them ideal for funds you will need within 18 to 24 months.