Why Cash Buyers Eliminate Financing Risk in Real Estate

TL;DR:

- Cash buyers eliminate financing risk by purchasing properties outright and avoiding lender approval or appraisals. They close faster, often within a week, and reduce contingencies, providing sellers with more certainty and less financial uncertainty. This makes cash offers especially valuable for homeowners facing urgent financial situations or deadlines.

Cash buyers eliminate financing risk by purchasing property outright, without relying on mortgage approval, underwriting, or lender-required appraisals. For homeowners facing financial distress or needing a quick sale, this distinction is the difference between a closed deal and a collapsed one. Traditional financed sales carry multiple points of failure: a buyer’s credit score drops, an appraisal comes in low, or a lender pulls approval at the last minute. Understanding why cash buyers eliminate financing risk gives you a clear path to a faster, more certain sale.

Why cash buyers eliminate financing risk at every stage

The mortgage process is the single biggest source of delay and uncertainty in a traditional home sale. A financed buyer must pass through credit checks, income verification, debt-to-income analysis, underwriting review, and a lender-ordered appraisal before closing. Each step is a potential failure point. Cash transactions close in 7–14 days, compared to 30–60 days for financed deals. When title is clear and documentation is ready, some cash deals close in as little as 72 hours.

The appraisal step alone causes significant problems in financed transactions. Lenders will not approve a loan for more than the appraised value of a property. If your home appraises below the agreed sale price, the buyer must either make up the difference in cash, renegotiate the price, or walk away. Cash buyers avoid appraisal contingencies entirely because their purchase price reflects what they are willing to pay, not what a lender will fund. That single difference removes one of the most common reasons traditional deals fall apart.

Mortgage underwriting adds another layer of risk. Underwriting is the lender’s process of verifying every financial detail about the buyer before releasing funds. It can take weeks, and lenders can deny a loan at any point during that period. Cash buyers skip underwriting completely. No lender is involved, so no lender can say no.

Pro Tip: Ask any cash buyer for a proof-of-funds letter before accepting their offer. A legitimate cash buyer can produce a bank statement or letter from a financial institution showing available funds within 24 hours.

How often does buyer financing actually fall through?

The failure rate for financed deals is higher than most sellers expect. Approximately 20% of financed deals face closing delays or cancellations specifically because of financing issues or appraisal gaps. That means roughly one in five traditional sales hits a serious obstacle before closing.

Common reasons a financed buyer’s deal collapses include:

- Job loss or income change between offer acceptance and closing, which triggers a lender to deny the loan

- Credit score drop caused by the buyer opening new credit accounts or missing a payment during escrow

- Appraisal gap when the property appraises below the contract price and neither party will adjust

- Debt-to-income ratio shift if the buyer takes on new debt before closing

- Lender-imposed condition that the buyer cannot satisfy within the required timeframe

Each of these scenarios puts you back to square one. You lose weeks of time, pay additional carrying costs, and re-list a property that buyers may now view as having a problem.

Cash buyers provide sellers with certainty of closure, which reduces the emotional and financial burden of waiting on loan approvals that may be denied at the last minute. For a seller already under financial pressure, that certainty is not a luxury. It is a necessity.

Sellers under financial distress benefit most from targeting cash buyers because fewer contingencies and faster closings directly address the time pressure they face. When you are dealing with foreclosure, mounting debt, or a life change that requires a fast move, a financed buyer’s 60-day timeline is not a workable option.

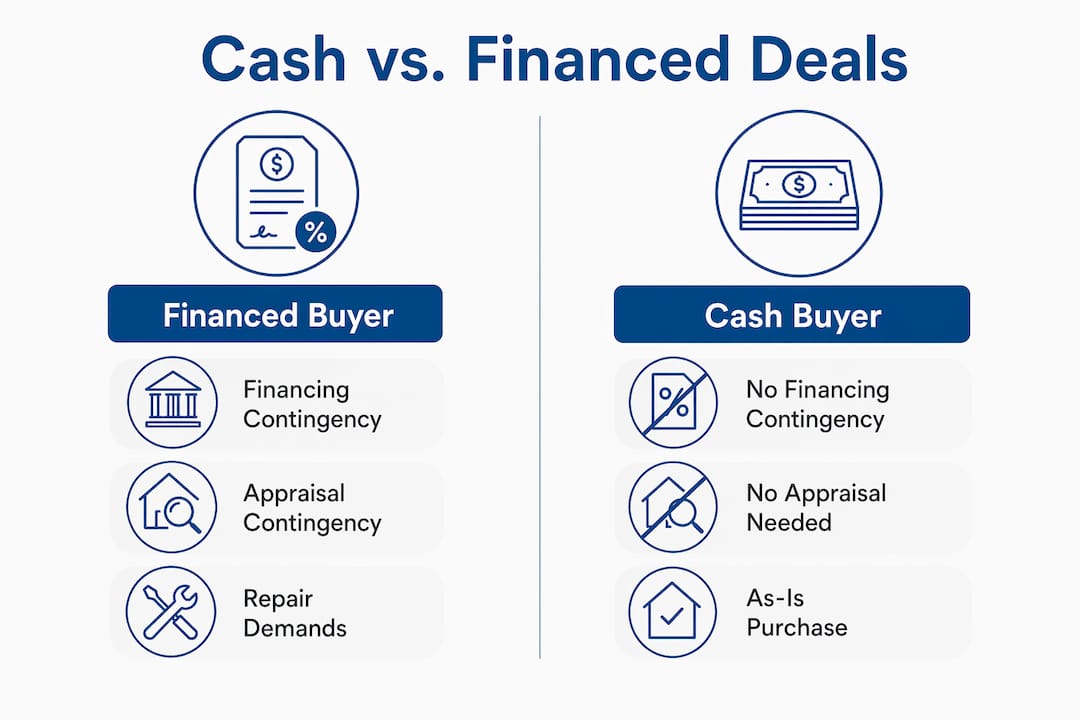

Contingencies in cash vs. financed deals: what changes for you?

Contingencies are conditions that must be met before a sale can close. Financed buyers typically bring three major contingencies to the table: a financing contingency, an appraisal contingency, and an inspection contingency. Each one gives the buyer a legal exit from the contract if conditions are not met.

A financing contingency means the buyer can walk away if their lender denies the loan. An appraisal contingency means the buyer can exit if the home appraises below the sale price. The role of appraisal in financed transactions is significant because lenders use it to set the maximum loan amount, which directly controls whether a deal survives. An inspection contingency means the buyer can request repairs or credits after a home inspection, or cancel the contract entirely.

Cash buyers typically reduce or eliminate all three. The table below shows how contingencies differ between the two buyer types.

| Contingency type | Financed buyer | Cash buyer |

|---|---|---|

| Financing contingency | Required by lender | Not applicable |

| Appraisal contingency | Required by lender | Typically waived |

| Inspection contingency | Common | Often waived or limited |

| As-is purchase | Rare | Common |

| Closing timeline | 30–60 days | 7–14 days |

Cash buyers often purchase properties in as-is condition, which removes seller repair demands entirely. For a homeowner who cannot afford to fix a roof or update an HVAC system before selling, this is a direct financial benefit.

One advantage sellers often overlook is scheduling flexibility. Cash buyers are not bound by lender-imposed occupancy or closing deadlines. That means you can negotiate a closing date that works for your timeline, or even arrange a rent-back agreement that lets you stay in the home for a period after closing. Financed buyers cannot offer this flexibility because their lender controls the closing schedule.

Pro Tip: If a cash buyer offers a lower price than a financed buyer, calculate the full cost of the financed deal. Add agent commissions, repair costs, carrying costs for 60 days, and the risk of the deal falling through. The cash offer often comes out ahead.

How to evaluate and protect yourself with cash offers

Receiving a cash offer is not the end of your due diligence. You still need to verify that the buyer actually has the funds and that the terms protect your interests.

- Request proof of funds immediately. Ask for a bank statement or a letter from a financial institution dated within the last 30 days. Do not accept a pre-approval letter, which applies only to financed buyers.

- Review the purchase agreement carefully. Even cash deals can include contingencies if the buyer inserts them. Read every condition before signing.

- Set a clear closing date in writing. Cash buyers can close quickly, but you should specify the exact date to avoid ambiguity.

- Understand the as-is terms. If the buyer is purchasing as-is, confirm in writing that no repair requests will follow the inspection.

- Compare net proceeds, not just offer price. Subtract any fees, commissions, or concessions from each offer to find your actual take-home amount.

Cash sales avoid many costs associated with traditional sales, including agent commissions, staging, repairs, and carrying costs during a long escrow. For homeowners who need to sell fast, those savings often offset a lower headline price. The benefits of a cash home sale go beyond speed. They include predictability, reduced paperwork, and fewer parties involved in the transaction.

In markets where speed is highly valued, cash offers give buyers a decisive advantage and sellers a reliable path to close. If you are facing a deadline, whether from a job relocation, a divorce, or a looming foreclosure, a cash buyer is not just convenient. It is the most practical option available.

Key Takeaways

Cash buyers eliminate financing risk by removing lenders, appraisals, and contingencies from the transaction, giving sellers speed, certainty, and control over the closing process.

| Point | Details |

|---|---|

| Cash deals close faster | Expect 7–14 days versus 30–60 days for financed sales, sometimes as fast as 72 hours. |

| Financing failure is common | Roughly 20% of financed deals face delays or cancellations due to financing or appraisal issues. |

| Fewer contingencies protect sellers | Cash buyers typically waive financing, appraisal, and inspection contingencies, reducing exit points. |

| As-is sales reduce seller costs | Cash buyers often purchase without repair demands, saving sellers money before closing. |

| Net proceeds matter more than price | Factor in commissions, repairs, and carrying costs before comparing cash and financed offers. |

What 16 years in real estate taught me about cash offers

Working in Detroit real estate for over a decade and a half, I have watched sellers make the same mistake repeatedly. They fixate on the highest offer price and ignore the probability of that offer actually closing. A financed offer at full asking price sounds great on paper. But if that buyer’s lender pulls approval three weeks before closing, you have lost time, money, and momentum.

The sellers who come out ahead are the ones who treat certainty as a form of value. A cash offer at 5% or 10% below asking price often delivers more money in the end once you subtract agent fees, repair concessions, and the cost of carrying a property for two additional months. The math is not complicated. The discipline to do it under pressure is what most sellers lack.

Cash offers also reduce the emotional toll of selling. Waiting on a lender’s decision while your financial situation worsens is genuinely stressful. Cash buyers remove that waiting period. You know within days whether the deal is done. That clarity has real value, especially for homeowners navigating foreclosure, job loss, or a health crisis.

My honest recommendation: if speed and certainty matter to you, prioritize verified cash offers. Do not let a higher number on a financed offer distract you from the risk attached to it. Evaluate every offer on its net outcome and its probability of closing. Those two factors will guide you to the right decision every time.

— Real Estate Team

Sell Dave Your House: fast cash offers for Detroit-area homeowners

Homeowners in Detroit and surrounding communities like Pontiac, MI deserve a straightforward path to selling without the uncertainty of financing contingencies.

Sell Dave Your House has over 16 years of experience buying homes directly for cash, with fair offers delivered within 24 hours and closings in as little as seven days. There are no agent commissions, no repair requirements, and no lender delays. Whether you are facing foreclosure, financial hardship, or simply need to move fast, Sell Dave Your House provides a clear, compassionate process from first contact to closing. If you are ready to see what your home is worth, get a fair cash offer today. You can also learn more about the reasons to sell fast and why so many Detroit homeowners choose this path.

FAQ

Why do cash buyers close so much faster than financed buyers?

Cash buyers skip lender approval, underwriting, and appraisals entirely. Without those steps, closing takes 7–14 days instead of the 30–60 days required for a financed sale.

What happens if a financed buyer’s deal falls through?

The seller loses weeks of time and must relist the property. Roughly 20% of financed deals face delays or cancellations due to financing failures or appraisal gaps.

Do cash buyers always pay less than financed buyers?

Cash offers are sometimes lower, but cash sales avoid costs like agent commissions, repairs, and carrying costs that reduce the net proceeds from a financed sale. The final numbers are often comparable.

How do I verify a cash buyer is legitimate?

Request a proof-of-funds letter or recent bank statement dated within 30 days. A genuine cash buyer produces this documentation quickly and without hesitation.

Can I negotiate closing dates with a cash buyer?

Yes. Cash buyers are not bound by lender-imposed deadlines, so you can negotiate a closing date that fits your schedule, including rent-back arrangements after closing.